Why a Stagnant China May Be More Dangerous Than a Rising One

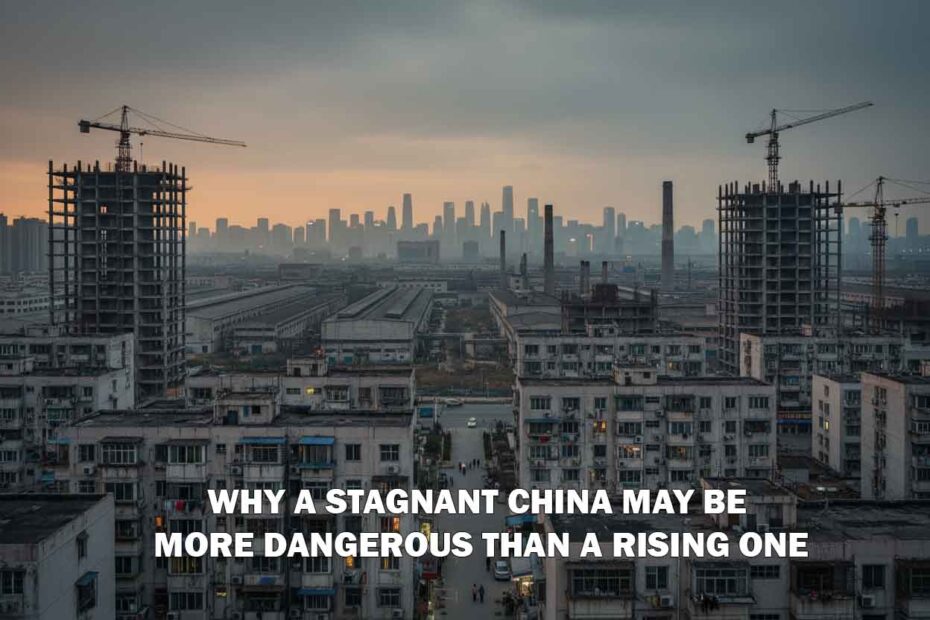

Imagine it is the year 2050. You are walking through a third-tier city in China, perhaps in the north-eastern rust belt. The sky is the now-familiar industrial grey, but something feels different. The streets are quiet – too quiet. A vast residential complex looms ahead, a thirty‑storey concrete relic from the boom years. It looks less like a vibrant housing project and more like a tombstone.

Half the windows are dark. Many of the rest are lit by a dim yellow glow, occupied almost entirely by people over the age of seventy. Children are nowhere to be seen. The Playgrounds are empty, the schools have been converted into nursing homes, and the factories that once produced cheap electronics for Western consumers stand silent, their machinery rusting for lack of young workers.

For decades, much of the world’s anxiety has centred on the rise of China: its growing military power, its technological ambitions, its seemingly inexorable economic ascent and its potential to eclipse the United States. Yet while attention was fixed on the skyscrapers and high‑speed rail lines, far less notice was paid to the structural weaknesses spreading beneath the surface.

The uncomfortable proposition is this: the greatest danger may not be an all‑conquering China, but a stagnating, frustrated and fearful one. A China that realises its economic and demographic peak has passed may become more volatile, not less. Instead of gliding into global leadership, it risks turning inward, lashing out externally and exporting instability.

This article explores the key fault lines behind the end of the so‑called “Chinese Dream”: demographics, debt, disillusioned youth, a collapsed property model, weakened local governments, broken social contracts, capital flight, technological strangulation, diplomatic overreach and the growing temptation to seek legitimacy through nationalism and external conflict.

The Demographic Time Bomb

China’s most profound problem is not political or ideological. It is mathematical. In 1980, fearful of Malthusian overpopulation and mass starvation, the Chinese Communist Party (CCP) implemented the one-child policy. The logic, at the time, seemed sound: reduce births, ease pressure on resources and concentrate national energy on economic development.

For around three decades this decision appeared to pay off. China enjoyed what economists term a “demographic dividend” – a large working-age population with relatively few dependants. This fuelled high savings, cheap labour and rapid industrialisation. The world’s factory was born.

However, biology eventually presents the bill. By forcibly suppressing births for so long, China has created an inverted population pyramid. The country is now entering the era of the “4:1 problem”: one working-age adult supporting two parents and four grandparents. For millions of only children now in their 20s and 30s, there are no siblings or cousins with whom to share this burden.

China’s population has already begun to shrink. Official figures show the total population started to decline in 2022 and the pace accelerated in 2023. More important than the headline total is the composition: the number of working-age people peaked around 2014 and has been falling since. By 2050, China is projected to lose around 200 million working‑age adults – the equivalent of erasing the entire workforce of a large continent‑sized country.

Layered on top of this is a severe gender imbalance. During the one‑child era, a strong cultural preference for sons led to the widespread abortion or abandonment of baby girls. The result is tens of millions more men than women of marrying age – sometimes referred to as “bare branches”: men who are statistically unlikely ever to marry or have children. Historically, large cohorts of unattached, frustrated young men have often correlated with higher risks of social unrest or external conflict.

The CCP is acutely aware of the crisis and has attempted to reverse course. The one‑child rule has been relaxed first to two children, then three. Campaigns urge citizens to marry younger and have more babies, sometimes in absurdly direct terms. Yet fertility has continued to fall. The cost of housing and child‑rearing in major cities rivals or exceeds that in many Western capitals, relative to income. After four decades of being told “one is enough”, and facing stagnant wages and enormous pressures, many young couples simply opt out of parenthood, or limit themselves to a single child.

Crucially, China is ageing before it has attained the per‑capita wealth of developed economies. When Japan entered its own demographic slowdown in the 1990s, it was already a rich country with robust social safety nets and high levels of savings. China’s GDP per capita remains closer to the level of a mid‑income state. Its pension system is underfunded, and studies suggest key pension funds could be exhausted within little more than a decade.

An ageing society with limited welfare capacity faces a vicious circle. As more resources are diverted to supporting the elderly, fewer remain to invest in education, innovation and productivity. Younger generations face rising tax burdens while struggling with high living costs and precarious jobs. Their ability and willingness to form families decline further, deepening the demographic spiral.

In short, the human engine that powered China’s economic miracle is stalling. No amount of rhetoric or coercion can conjure millions of missing young adults into existence.

The Property Bubble and the “Ghost City” Economy

If demographics are China’s long‑term gravity, property is its immediate fault line. For roughly two decades, Chinese growth was underpinned by an enormous real estate boom. In a system with restricted avenues for domestic investment, tight controls on capital outflows and a stock market distrusted by ordinary savers, property became the default store of wealth.

Households in China hold a far greater proportion of their assets in housing than their counterparts in most Western economies. The idea that “property always goes up” became a quasi‑religious belief and an implicit part of the regime’s legitimacy.

The dominant property model was the “pre‑sale”: buyers paid in full – or committed to long‑term mortgages – for flats that had not yet been built. Developers used this cash not only to construct the promised units, but also to acquire new land and take on additional loans. Rising prices made the whole system appear sustainable.

It was, in effect, a nationwide pyramid scheme. At its height, real estate and related sectors accounted for close to a third of China’s GDP. Estimates suggest there may be tens of millions of empty housing units across the country – enough to accommodate entire large nations. Vast “ghost cities”, lined with high‑rise blocks and empty shopping centres, bear witness to this over‑building.

When Beijing belatedly recognised that developer debt was spiralling out of control, it tightened credit conditions and imposed new limits on borrowing. This punctured the bubble. Large developers defaulted. Construction on countless pre‑sold projects simply stopped.

For millions of families, the consequences are devastating. They are servicing mortgages on flats that exist only as concrete shells. In some cases, people have moved into partially built blocks with no lifts, no heating and no running water, simply because they have nowhere else to go and cannot abandon the asset that holds their life savings.

A property sector that once symbolised rising prosperity is now a source of anger and betrayal. With so much household wealth concentrated in real estate, a sustained fall in prices is not simply a cyclical correction; it is a direct hit to social stability. The Party‑state’s unspoken compact – economic betterment in exchange for unquestioned political control – comes under strain when ordinary people see their nest eggs disintegrating.

Attempts to stabilise the sector through lower interest rates, relaxed purchasing restrictions and moral suasion on banks have so far struggled to rebuild confidence. Once faith in perpetual appreciation is broken, buyers are understandably reluctant to commit to the largest purchase of their lives in an environment of unfinished buildings and insolvent developers.

Youth Disillusionment: “Lying Flat” and “Letting It Rot”

Economic stress is not confined to bricks and mortar. It is increasingly psychological. Among young Chinese, three concepts have gained currency: involution, “lying flat” and “letting it rot”. Each captures a distinct layer of disaffection.

“Involution” describes a hyper‑competitive, zero‑sum society in which everyone is working harder, yet nobody seems to be progressing. From early childhood, many Chinese students endure punishing study schedules aimed at passing the fiercely competitive university entrance examinations. The prize for surviving this ordeal used to be a decent job and a path into the middle class.

Today, even elite graduates often struggle to find secure employment in the formal economy. Many end up in low‑status service roles or in precarious gig work, despite years of education and sacrifice.

“Lying flat” emerged as a quiet rebellion against this treadmill: a conscious decision to reject conventional aspirations of property ownership, marriage, children and corporate advancement. Instead, adherents embrace minimalism and low consumption, working only as much as necessary to subsist.

The more nihilistic evolution of this mood is captured by the phrase “let it rot”: the sense that the system is beyond repair and any effort to improve one’s situation is futile. Indicators of youth distress are stark. Reported unemployment among 16‑ to 24‑year‑olds has at times reached levels that would alarm any government. When the data became politically embarrassing, authorities simply stopped publishing it for a period, before later revising the methodology.

This is not only a social issue; it is an economic one. Innovation and entrepreneurship rely on optimism and a perception of opportunity. A generation that has mentally checked out – or is preoccupied with bare survival and family obligations – is unlikely to launch high‑growth companies, take creative risks or commit to having multiple children.

The official response has often been tone‑deaf: exhortations from ageing leaders to “eat bitterness” and embrace hardship, or propaganda stories celebrating graduates who find fulfilment in menial work. For young adults facing a world of unaffordable housing, insecure work and shrinking horizons, such messaging only underlines the gulf between their reality and the leadership’s narrative.

Local Government Debt and the Hollowing of the State

Behind the visible property bust lies a more hidden but equally serious debt crisis at the local government level. China’s fiscal architecture is peculiar. The central government collects the bulk of tax revenue, yet local and provincial authorities are responsible for most public spending on healthcare, education, infrastructure and basic services.

Unable to borrow directly in the normal way, local governments created off‑balance‑sheet financing vehicles. These entities took ownership of public land, used it as collateral to secure loans, and invested the proceeds in construction projects ranging from roads and metro systems to industrial parks and prestige buildings. Rising land values and buoyant property sales made this model viable for a time.

The property downturn has shattered the illusion. Land sales – which provided a huge share of local revenues – have collapsed. The projects funded by the earlier borrowing often generate little to no cash flow. Debt servicing costs mount, while income declines.

The result is an enormous pile of opaque liabilities at the local level, potentially running into many trillions of dollars. In practice, this manifests in delayed wages for teachers and civil servants, cuts to basic services and emergency appeals to Beijing for bailouts or debt swaps.

When local governments are forced into austerity, they can no longer play their previous role as engines of investment and employment. The knock‑on effects on small businesses, construction companies and regional economies are severe. Even more worrying for the CCP, the visible fraying of local services undermines one of its core claims: that one‑party rule guarantees order, competence and stability.

Central authorities have begun converting some of this shadow debt into formal government bonds, effectively shifting the problem from one balance sheet to another. However, this is largely a bookkeeping exercise. The underlying reality remains: years of over‑building and malinvestment have left a legacy of concrete assets with dubious economic value, and the bill must eventually be paid.

The Consumption Trap and Deflationary Pressures

For years, both Chinese and Western policymakers argued that China could transition from an investment‑ and export‑led growth model to one driven more by domestic consumption. In theory, a vast and growing middle class would sustain demand even as external markets matured and manufacturing costs rose.

In practice, that transition has stalled. Household consumption makes up a much smaller share of China’s GDP than in most advanced economies. Chinese citizens save at extraordinarily high rates. This is not simply a cultural quirk; it is a rational response to insecurity.

Three major pressures dominate the financial lives of many urban families: housing costs, educational expenses and healthcare risks. The first has already been discussed. The second is driven by intense competition for good schools and universities, pushing parents to spend heavily on tutoring and enrichment, even when such services are formally restricted. The third stems from a healthcare system that, while improving, still leaves families exposed to potentially ruinous bills for serious illness.

In such an environment, households are reluctant to spend freely on discretionary goods and services. The scars of harsh pandemic lockdowns have only reinforced this cautious instinct. Rather than a burst of “revenge spending” after restrictions eased, China saw a surge in precautionary savings as people grappled with the arbitrary nature of local lockdowns, sudden business closures and the realisation that income could vanish overnight.

Weak consumer confidence and subdued spending have contributed to deflationary pressures: falling or flat prices in several sectors. While low inflation might sound benign, persistent deflation can be deeply damaging. If people expect prices to fall further, they postpone purchases, which suppresses demand, lowers corporate revenues and can trigger lay‑offs – reinforcing a vicious circle of pessimism and under‑consumption.

Beijing’s policy response has largely focused on stimulating supply – encouraging banks to lend, nudging factories to produce and promoting exports. It has been far more reluctant to engage in straightforward redistribution to households, such as direct cash transfers or large‑scale social spending increases, partly out of ideological discomfort with anything perceived as “welfarism”.

The consequence is an economy that can churn out more goods than its citizens wish or are able to buy, forcing surplus production onto global markets. This fuels trade tensions and, increasingly, retaliatory tariffs, particularly in sectors like electric vehicles and renewable energy equipment.

The Squeezing of the Private Sector

Even as domestic demand falters, China is constraining one of its greatest historical strengths: an energetic private sector. For much of the 2000s and 2010s, Chinese internet and technology companies were among the most dynamic in the world. Digital platforms transformed payments, logistics, retail, transport and everyday life.

However, this flourishing of entrepreneurial power created unease at the top of the political system. Large technology companies accumulated vast troves of data, influence over consumers and a degree of cultural prestige. Charismatic founders became national and international celebrities.

Over the last few years, the Party has reasserted control over the private sector through a series of regulatory crackdowns, fines, forced restructurings and the imposition of “golden shares” – small equity stakes that confer outsized control rights to state entities. Entire industries, such as private tutoring, have been all but wiped out overnight by sudden policy edicts.

The message to entrepreneurs is clear: success is tolerated only so long as it aligns with the Party’s priorities and does not challenge its authority or narrative. Property rights are contingent. Scale itself invites suspicion.

This environment chills risk‑taking. Ambitious founders either redirect their efforts into state‑favoured fields such as semiconductors, electric vehicles or defence‑related technologies, or they simply look abroad. Many of the most internationally minded and capable businesspeople are engaged in precisely that calculation: whether to continue building in China, or to quietly shift capital and talent overseas.

Capital Flight and the “Run” Mentality

Capital does not argue; it leaves. In recent years, significant numbers of high‑net‑worth individuals have relocated assets and, where possible, their families to jurisdictions deemed safer and more predictable – such as Singapore, parts of Europe, Japan or North America.

This phenomenon is colloquially discussed in China under the term “run” – not merely as physical emigration but as the strategic withdrawal of wealth from a system perceived as increasingly arbitrary. Official capital controls limit the legal transfer of funds abroad, so a whole ecosystem of workarounds has emerged, ranging from legalistic structures to dubious grey‑market schemes.

It is not only the very rich who seek escape. Growing numbers of middle‑class citizens, professionals and small business owners, disillusioned with domestic prospects, have embarked on arduous migration routes through third countries in Latin America and elsewhere, aiming ultimately for Western destinations.

This outflow of human and financial capital represents a vote of no confidence in the country’s trajectory. It undermines longer‑term growth by siphoning away precisely the segment of society most capable of driving innovation, investment and reform.

The Middle‑Income Trap and Educational Limits

At a macro level, China appears to be encountering the “middle‑income trap”. It has successfully transitioned from agrarian poverty to industrial middle‑income status, but is finding it far harder to become a fully fledged high‑income, innovation‑driven economy.

A critical constraint lies in human capital. While China has world‑class universities and research institutes in some cities, the overall education level of its workforce remains uneven. A large proportion of adults have not completed upper‑secondary education. Deep structural divides persist between urban and rural areas, and the household registration system (hukou) entrenches these inequalities by limiting access to high‑quality schools and public services for migrant families.

Many of the low‑skill manufacturing jobs that once absorbed rural migrants are increasingly automated or relocated to cheaper countries. Yet a substantial portion of the workforce lacks the training to move into higher‑skill sectors. Simultaneously, university graduates often find themselves over‑qualified for the roles actually available, fuelling frustration and under‑employment.

This mismatch between educational attainment, labour‑market demand and institutional barriers hampers productivity growth. Without sustained improvements in both the quantity and quality of education – particularly in rural areas – China may struggle to sustain the knowledge‑intensive industries needed to escape the middle‑income trap.

Technological Containment and the “Silicon Curtain”

China’s aspiration to lead in fields such as artificial intelligence, advanced manufacturing and military technology depends heavily on access to cutting‑edge semiconductors and the tools required to produce them.

In recent years, the United States and certain allies have imposed far‑reaching export controls on advanced chips, manufacturing equipment and the expertise required to operate them. These measures aim explicitly to slow or cap China’s progress in sensitive technologies, particularly those with military applications.

China still imports a very large share of its high‑end chips. Efforts to build a fully independent, world‑class semiconductor ecosystem face formidable technical, managerial and geopolitical obstacles. While domestic firms have made incremental advances – including producing somewhat more advanced chips with older-generation tools – the gap with global leaders remains wide and may continue to widen as others move to even smaller and more sophisticated process nodes.

This technological “ceiling” complicates China’s growth prospects. Without ready access to top-tier computational hardware, it becomes harder to train frontier AI models at scale, develop next‑generation defence systems or compete at the very top of the value chain in digital industries. Enormous sums are being poured into domestic substitutes, but money cannot instantly compensate for decades of accumulated know‑how, intellectual property and network effects held by foreign firms.

Belt and Road: From Grand Strategy to Overstretch

Externally, China’s most ambitious economic diplomacy project has been the Belt and Road Initiative: a vast web of infrastructure lending and construction across Asia, Africa, Europe and Latin America. It was intended both to secure trade routes and resources, and to increase Beijing’s geopolitical influence by binding partner countries into long-term economic relationships.

A decade on, the record is mixed at best. Several recipient countries are burdened with heavy debts for projects of questionable economic viability. Some high‑profile schemes – ports, power plants, railways – have failed to generate the expected revenues. In other cases, political backlash has emerged over terms perceived as opaque or unfavourable, and over the influx of Chinese labour and environmental impacts.

For China itself, the costs of supporting struggling borrowers have mounted. In effect, Beijing has found itself acting as a lender of last resort to its own clients, restructuring loans and offering new credit simply to prevent defaults that would crystallise losses or damage its reputation. Recent rhetoric from Chinese leaders has noticeably downshifted from grand visions of transcontinental transformation to more modest talk of “small and beautiful” projects.

Rather than a seamless new Silk Road radiating prosperity, the Belt and Road risks becoming a network of strained relationships, sunk costs and politicised assets of limited strategic value. At a time when China faces intense domestic economic pressure, continuing to pour resources into such ventures generates resentment at home as well as scepticism abroad.

Surveillance, Control and the Erosion of Trust

As economic levers weaken, the CCP has redoubled its reliance on surveillance and coercive control to maintain order. China has constructed one of the most extensive digital panopticons on earth: vast networks of cameras, biometric databases, algorithmic monitoring of online behaviour and integrated data platforms designed to map and predict citizens’ activities.

A patchwork of “social credit” mechanisms and blacklists restricts access to transport, finance or education for those deemed untrustworthy or politically problematic. Predictive policing tools attempt to identify potential “troublemakers” before they act, based on patterns in their communications, movements or consumption.

At the local level, grid management systems subdivide neighbourhoods into small units overseen by quasi‑official watchers, tasked with reporting on anything from unauthorised religious gatherings to domestic disputes.

These measures can suppress visible dissent and deter organised opposition. However, they do not generate genuine loyalty or enthusiasm. Instead, they foster cynicism, self‑censorship and a pervasive sense of insecurity. When people assume they are always observed, they retreat into smaller circles of trust, avoid discussing sensitive topics and become more reluctant to take initiative in any sphere that might be politically misinterpreted.

Such an atmosphere is inimical to the open exchange of ideas and trial‑and‑error experimentation that underpin creativity and innovation. It may keep the current regime in place in the short term, but at the cost of stifling the very dynamism required to navigate a complex, slowing economy.

Strategic Vulnerabilities: Food, Energy and Geography

Beneath the high‑tech surface, China remains acutely vulnerable in basic material terms. It has a large population relative to its arable land and suffers from significant environmental degradation. The country is heavily dependent on imports of key commodities, particularly foodstuffs such as soybeans and energy resources such as oil and gas.

Much of this trade flows through maritime chokepoints, notably the Strait of Malacca. In a major conflict, adversaries would not need to invade the mainland to exert devastating pressure. Disrupting seaborne supply routes could rapidly inflict shortages of fuel and raw materials, curtailing industrial output, transport and ultimately food distribution.

This structural dependence helps explain Beijing’s assertive behaviour in the South China Sea, its pursuit of alternative pipeline routes across Central Asia and Pakistan, and its sometimes heavy‑handed approach to upstream water resources on major rivers. From the leadership’s perspective, securing access to resources is not simply an economic issue; it is existential.

However, attempts to mitigate vulnerability through territorial claims, militarisation of disputed waters or control over critical infrastructure in other states have contributed to diplomatic backlash and growing alignment among regional neighbours who feel threatened.

Diplomatic Overreach and Growing Isolation

For many years, China’s foreign policy was guided by the principle of “hiding one’s strength and biding one’s time”. This relatively low‑key approach helped reassure other countries that China’s rise was not an immediate threat and encouraged trade and investment flows.

In the past decade, that posture has shifted. A more strident diplomatic style, often described as “wolf warrior” diplomacy, has seen Chinese officials engage in public confrontations, sharp rhetoric and economic coercion against states that criticise Beijing or diverge from its preferred positions.

The results have frequently been counter‑productive. Countries in Europe, Asia and Oceania that once viewed closer ties with China primarily in commercial terms now increasingly frame their relationship in strategic and security language. Coalitions and defence arrangements that might once have seemed unlikely – among Japan, South Korea, Australia, India, the United States and others – have gained momentum, driven in no small part by anxiety over Beijing’s behaviour.

Even where economic ties remain substantial, trust has eroded. Many governments now see engagement with China as something to be hedged against through diversification of supply chains, greater scrutiny of Chinese investment and strengthened alliances. This, in turn, feeds Beijing’s sense of encirclement and grievance, reinforcing nationalist narratives and the belief that hostile forces aim to contain China’s rightful rise.

The Peak Power Trap: Why Stagnation Increases Risk

Bringing these strands together, a picture emerges of a country facing simultaneous headwinds: a shrinking and ageing population, a bursting property bubble, indebted local governments, cautious consumers, constrained private enterprise, technological containment, resource insecurity and mounting diplomatic pushback.

This is not the profile of a self‑confident, rising hegemon. It is the profile of a state that suspects its moment of maximum relative power may already be passing.

History suggests that such moments can be especially dangerous. Rising powers that believe time is on their side often prefer stability. They can afford patience, knowing that continued growth will only improve their position. Powers that sense they have peaked, by contrast, may be more inclined to take bold risks while they still possess significant military and economic strength.

This logic is sometimes described as the “peak power trap”. It does not predetermine conflict, but it raises the probability of miscalculation. When leaders face domestic pressures they cannot easily relieve through growth – unemployment, inequality, disillusionment – the temptation to seek legitimacy through nationalism, external confrontation or “historic missions” increases.

In China’s case, the most obvious focal point for such a mission is Taiwan. The island holds deep symbolic meaning in CCP narratives of national rejuvenation. It also sits astride critical sea lanes and houses the world’s most advanced semiconductor manufacturing facilities. Any serious attempt by Beijing to force “reunification”, whether through blockade, coercive pressure or outright invasion, would create the greatest geopolitical crisis in decades and carry immense risks of escalation.

At the same time, one should not underestimate the dangers of a disorderly internal collapse. The CCP has systematically undermined alternative centres of organisation in society – independent unions, religious institutions, civic associations – that might otherwise facilitate a relatively peaceful political transition. A power vacuum in a nuclear‑armed, continent‑sized country with deep social and regional divides could unleash chaos on a scale unprecedented in modern history, with profound global economic and security implications.

Conclusion: Living with a Wounded Giant

The narrative that dominated much of the early 21st century – of an ever‑rising China destined to overtake the United States and reshape the global order – no longer fits the emerging realities. Yet the alternative narrative, of an imminent Chinese collapse that neatly resolves strategic anxieties, is equally misleading and potentially dangerous.

A more sober assessment recognises that China is entering a prolonged period of structural slowdown and internal strain. Its leadership will remain powerful and capable of imposing order at home, but it will grapple constantly with the constraints of demography, debt, diminishing returns on investment and fading public optimism.

This combination – strength without confidence, power without a clear path to renewed prosperity – is precisely what makes a stagnant China potentially more hazardous to global stability than a smoothly rising one. It might act unpredictably abroad to compensate for frustrations at home. It might export economic volatility through over‑capacity and deflationary pressures. It might double down on repression and information control, making misjudgements more likely in the absence of honest feedback.

For the rest of the world, the task is delicate. On the one hand, there is a legitimate need to protect national security, diversify supply chains, defend smaller states from coercion and uphold norms against aggression. On the other, there is a clear interest in avoiding either a catastrophic conflict or a chaotic implosion in a country so deeply woven into global trade, finance, manufacturing and technology.

China is too large, too interconnected and too important for its internal trajectory to be a matter of indifference. The end of the Chinese Dream, at least in its original form of unbroken rapid ascent, does not mean the end of China’s central role in the world. Instead, it marks the beginning of a more complex and turbulent chapter in which the international system must adapt to living alongside a wounded, wary and still formidable giant.

Frequently Asked Questions

What is the “4:1 problem” and why does it pose such a significant threat to the Chinese economy? The 4:1 problem refers to a demographic crisis where a single working-age adult, typically an only child resulting from the one-child policy, is financially and socially responsible for two parents and four grandparents. This creates an inverted population pyramid that places an immense burden on the younger generation, diverting their income away from consumption and investment toward elder care. Mathematically, this leads to a shrinking workforce and a massive pension deficit, as there are fewer workers to support a rapidly ageing population, ultimately stalling the economic engine that powered China’s previous growth.

How did the Chinese property market transform from a national engine of wealth into a “Ponzi scheme”? For decades, real estate accounted for roughly 30% of China’s GDP, driven by a “pre-sale” model where citizens paid in full for apartments before they were built. Developers used this upfront cash to buy more land and take on further debt rather than simply completing existing projects, creating a cycle that relied on ever-rising prices and constant new investment. When the government introduced stricter borrowing limits to cool the market, the flow of easy credit stopped, causing major developers to default and leaving millions of families paying mortgages on “rotten tail” buildings—unfinished concrete shells that represent the loss of their life savings.

What do the terms “lying flat” and “letting it rot” reveal about the mindset of China’s younger generation? These terms describe a psychological rebellion among young people who feel trapped in a hyper-competitive “rat race” with diminishing returns, known as involution. “Lying flat” (Tangping) is a form of passive resistance where individuals reject traditional milestones like marriage, children, and career advancement in favour of a minimalist lifestyle. “Letting it rot” (Banan) is a more nihilistic stage of surrender, where the youth, facing record-high unemployment and unaffordable housing, simply give up on striving altogether. This widespread disillusionment creates a productivity void that makes it nearly impossible for the state to transition into a high-tech, consumption-led economy.

Why is a stagnating China considered more dangerous to global security than a rising one? This concept is rooted in the “peak power trap,” which suggests that a rising power is often cautious because time is on its side, whereas a power that has peaked and begun to decline becomes unpredictable and prone to risk-taking. If the Chinese Communist Party can no longer provide the economic growth that underpins its legitimacy, it may turn to aggressive nationalism and external conflict—such as a move against Taiwan—to distract the domestic population and unify the country. A wounded superpower that feels its window of opportunity is closing is more likely to gamble on military action before its demographic and economic rot makes such action impossible.

What is the “Silicon Curtain” and how does it impact China’s future ambitions? The Silicon Curtain refers to the sweeping export controls and trade barriers imposed by the United States and its allies to restrict China’s access to advanced semiconductors and chip-making equipment. Since modern power—including AI, autonomous weaponry, and advanced computing—depends on these high-end chips, being cut off from Western technology traps China in a technological past. While Beijing is investing billions to develop a domestic supply chain, the lack of access to cutting-edge tools like EUV lithography means they are struggling to innovate at the same pace as the West, effectively capping their ability to lead the next industrial revolution.